FOR NRI’s: FCNR (Foreign Currency Non-Resident)

The RBI extended full hedging-cost support for banks raising three- to five-year FCNR(B) deposits till September 30, 2026. FCNR(B) deposits are foreign currency deposits raised by banks from non-resident Indians.

Banks are offering 6-7% annual interest (in dollar terms) for a 3-5 yrs FD (FCNR). the scheme is open till 30th September 2026.

Over the last 10 years, the Indian Rupee (INR) has depreciated by approximately 37%, sliding from around ₹67 per US Dollar (USD) in early 2016 to hit historic lows breaching the ₹95 mark in mid-2026. This translates to a steady long-term annual decline of about 3%-to-4% against the dollar.

So while in dollar terms you get 7%, but in rupee terms, you could get 10-11% annual returns…and there is NO tax as it will be in FCNR/NRE account.

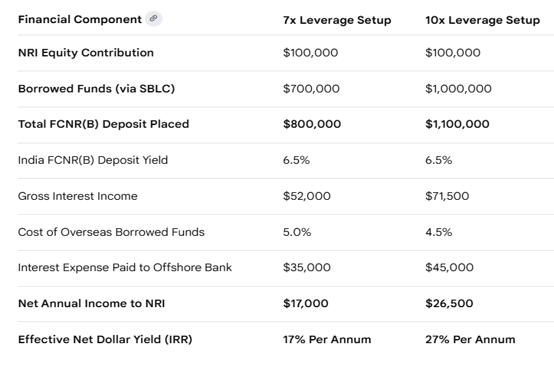

Also, here is a trick to enhance the 7% to 20%+ returns

In countries where you can get loan at lower interest rates. You can leverage up to 10 times to get very high interest rates. You can raise capital/take loan through SBLC route and increase your returns to 25%.

A Standby Letter of Credit (SBLC or SLOC) is a bank’s official guarantee of payment to a seller if the buyer defaults on a contractual obligation. It acts as a safety net of last resort to build trust in large international or domestic transactions.

So, you can get SLBC from your Indian bank and get the loan from international bank. Below is table explaining the returns…

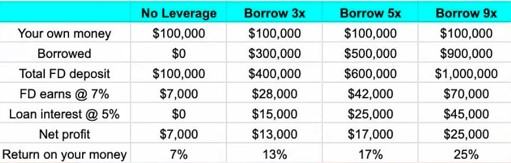

Here is another example…